The future of globalisation: a history

The future of globalisation: a history

One for the enthusiasts: a 5,500 word lecture I recently delivered at the University of Tokyo, arguing that (pace Solow) we can see deglobalisation everywhere except in the trade statistics

I am delighted to again be invited to give this public lecture at the excellent Tokyo College. I have had the great honour to have been an Ushioda Fellow here at Tokyo College since this very special institution’s inception in 2019. As many will know, my principal obligation as an Ushioda Fellow is to deliver one public lecture each year. Although my time as an Ushioda Fellow began more than five years ago, this is only my fourth such public lecture thanks to the unfortunate intervention of the coronavirus pandemic.

The topic of my first lecture in 2019, “Envisioning a far more female future for Japan”, reflected the work I had been doing for a book with almost the same name that was published in Japanese in that same year and English in 2020, and conveyed my sense of the welcome social and economic changes that I felt were under way.

The next two lectures were much more international in their topics, though both reflected concerns which deeply affected Japan. In May 2022, my lecture title was “Trade War, Pandemic, the War in Ukraine: What we know, and don’t know, about the new political and economic order”. The focus, if that is the right word for such a broad set of concerns, was on the way in which “radical uncertainty” has come to characterise the world we inhabit, and on how in such a world preparation for a range of eventualities was much more likely to be relevant than attempting to predict what was going to happen and when.

In July 2023, I continued with this theme of preparation rather than prediction, except that I looked more specifically at the task for deterrence and diplomacy in the Indo-Pacific if war is to be avoided over Taiwan. This very much reflected the big change in Japan’s national security and defence strategy that had been announced by the government just half a year earlier in December 2022, albeit that that announcement represented a culmination of thinking about threats and responses during the previous decade.

The 2023 lecture also formed part of my efforts to think through these geopolitical and military issues for a book which will be published in Japanese by Fusosha Publishing in July under the title of “How to Stop World War Three”, and in English that same month by the International Institute for Strategic Studies, in their “Adelphi” series, under the rather more sober and academic title of “Deterrence, Diplomacy and the Risk of Conflict over Taiwan”. I thank Tokyo College warmly for the part that giving that public lecture played in my work on that book.

There is, I think, a clear link between those 2022 and 2023 lectures and my chosen theme this year. The link is the way in which changing geopolitics and socio-economic convulsions are shaking up what has been thought of as the international rules-based order, though not just shaking the rules but also seeming to make the economic outcomes look even more uncertain than they already were. As a result of that “radical uncertainty” about what might happen, in my view it is unwise to make firm predictions or judgements, but rather it is better to prepare for a range of potential outcomes and developments.

This kind of embrace of uncertainty does not come easily or naturally to us human beings. We all crave clarity and simplicity, whether we are the media, scholars, politicians, policy-makers or journalists. So we often find ourselves using or at least hearing simple words or phrases to describe the era through which we are passing, words which encapsulate a form of prediction or judgement. The word which acted as a catalyst for my lecture today is “deglobalisation”.

That word, which is being widely used as a description of our current age, can even take more extreme forms. I recently acted as discussant – the role kindly being taken for my lecture today by Professor Shimazu – at a talk in London being given by a Dutch analyst for the Atlantic Council called Elisabeth Braw, who has just published a book with a quite definitive title: “Goodbye Globalisation: The Return of a Divided World”.

While it is clear that in many senses the world is indeed now more divided than it was a decade or more ago, Ms Braw is arguing for something more: that the phenomenon we called “Globalisation”, the growing interconnectedness of most countries on the planet by trade, finance, ideas and technology, is a thing of the past. We have to say goodbye to it.

The question which I plan to address in this lecture is whether this idea, that we have to say “goodbye” to globalisation, is the right way to think about what is happening and what might happen. Or, more strictly, I plan to ask what factors and forces might determine whether this idea, which is in fact a forecast, will come to be both true and meaningful. I will do this by drawing on some other times in history when forecasts or judgements have been made about the future of globalisation. We therefore have the advantage of hindsight in knowing whether those forecasts turned out to be accurate, and what actually happened instead.

In choosing this approach and this title, I must acknowledge my debt to a great British scholar of war studies, Sir Lawrence Freedman, and the title of a book he published in 2017: “The Future of War: A History”.

Freedman’s object was not to show how previous expectations about war turned out to be wrong, though many were, but rather to examine how those expectations had been shaped and what factors, in hindsight, turned out to shape the evolution of war. I think we can do something similar with globalisation, even if my survey today of “the future of globalisation” is necessarily much less comprehensive than Freedman’s was of war, for the simple reason that globalisation is a far more recent phenomenon than war. Yet the reason why it is a much newer idea is itself indicative, which I shall come to later.

First, let us return to the idea that we are in an age of deglobalisation. I am tempted to say that this must be true, for The Economist, with which I was for many years associated, has just declared that the world’s economic order is breaking up and that deglobalisation is under way. Its thesis brings to mind Ernest Hemingway’s phrase about how one of his characters went bankrupt: gradually and then suddenly.

That notion is certainly becoming common. At the board of an institution which I chair in London, I heard this same idea used recently by the specialists who manage our institution’s endowment investments. Their key investment themes, they told us, are now three Ds: Deglobalisation, Decarbonisation and Demography.

It has long been clear that the prefix ‘DE’, meaning the reversal or removal of something, has become a theme of public policy in response to geopolitical tensions. China and the United States have both spoken about their desire to “De-couple” their economies by reducing or even eliminating some of the financial, technological and commercial connections between them. Diplomats, especially those who want to reassure corporate executives, have more recently replaced “de-couple” with the word “de-risk”, to show that this is not about complete separation but rather about reducing elements that could be risky in the event of some political shock equivalent to the 2022 Ukraine war.

Nonetheless, both de-coupling and de-risking are quite a reversal for two economies which were labelled by the historian Niall Ferguson and the economist Moritz Schularick as “Chimerica” in 2006, so intertwined did these scholars believe these two economies of China and America were becoming.

To some in the audience this idea may be reminiscent of ‘Nichibei’, the notion of American-Japanese interconnectedness that was briefly popular in the 1980s, with a similar idea behind it: that high Japanese savings were forming a perfect match with high American consumption. Yet in that reminiscence there also lies a clue to the fragility of these convenient phrases, or soundbites: just as Nichibei vanished from use rather quickly once the bursting of Japan’s economic bubble occurred in 1990, so Ferguson and Schularick soon pronounced “The End of Chimerica” in an article in the Harvard Business Review in 2009.

That death notice was in one sense quite prescient, for it stated, accurately as we now know, that the global financial crisis of 2008-09 was likely to put an end to the clear connection between Chinese over-saving and huge capital exports, and American over-consumption.

In another sense, however, we might wonder whether the speed of this death notice, just three years after the phenomenon had been given its catchy name, might cast doubt on whether the phenomenon itself had any real meaning in the first place.

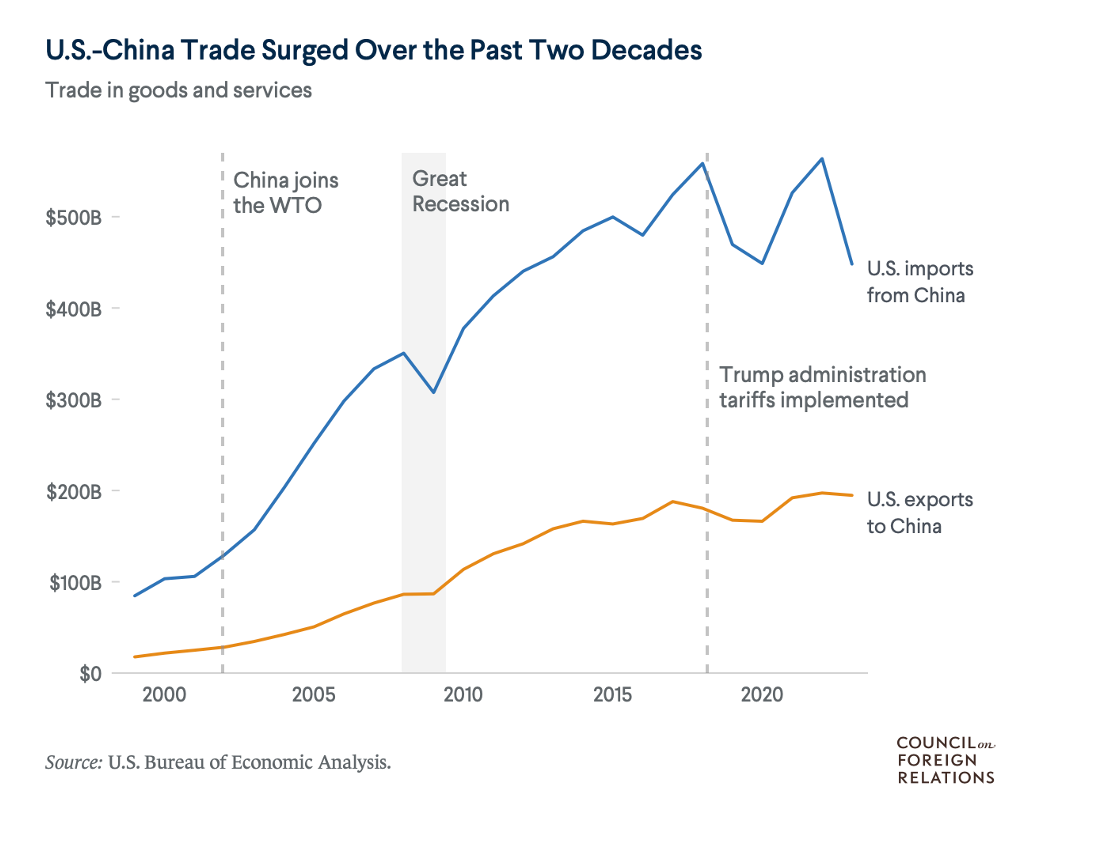

Let’s look at this graph of US-China trade taken from the Council on Foreign Relations in New York. Does this show either Chimerica in 2006 or the end of it after 2009? Well, the graph naturally shows a downturn in trade in the post-financial crisis recession, but then normal Chimerica service was soon resumed with two-way trade still growing quite strongly.

Then at around 2018-20 we see some obvious fluctuations in two-way trade first when the Trump administration imposed 25% tariffs on most imports from China, then with the pandemic recession, and more recently with further restrictions being imposed by the Biden administration. However, US exports to China have been relatively stable during this whole period, even though China imposed its own retaliatory tariffs and the US has placed controls over high-technology exports to China on national security grounds.

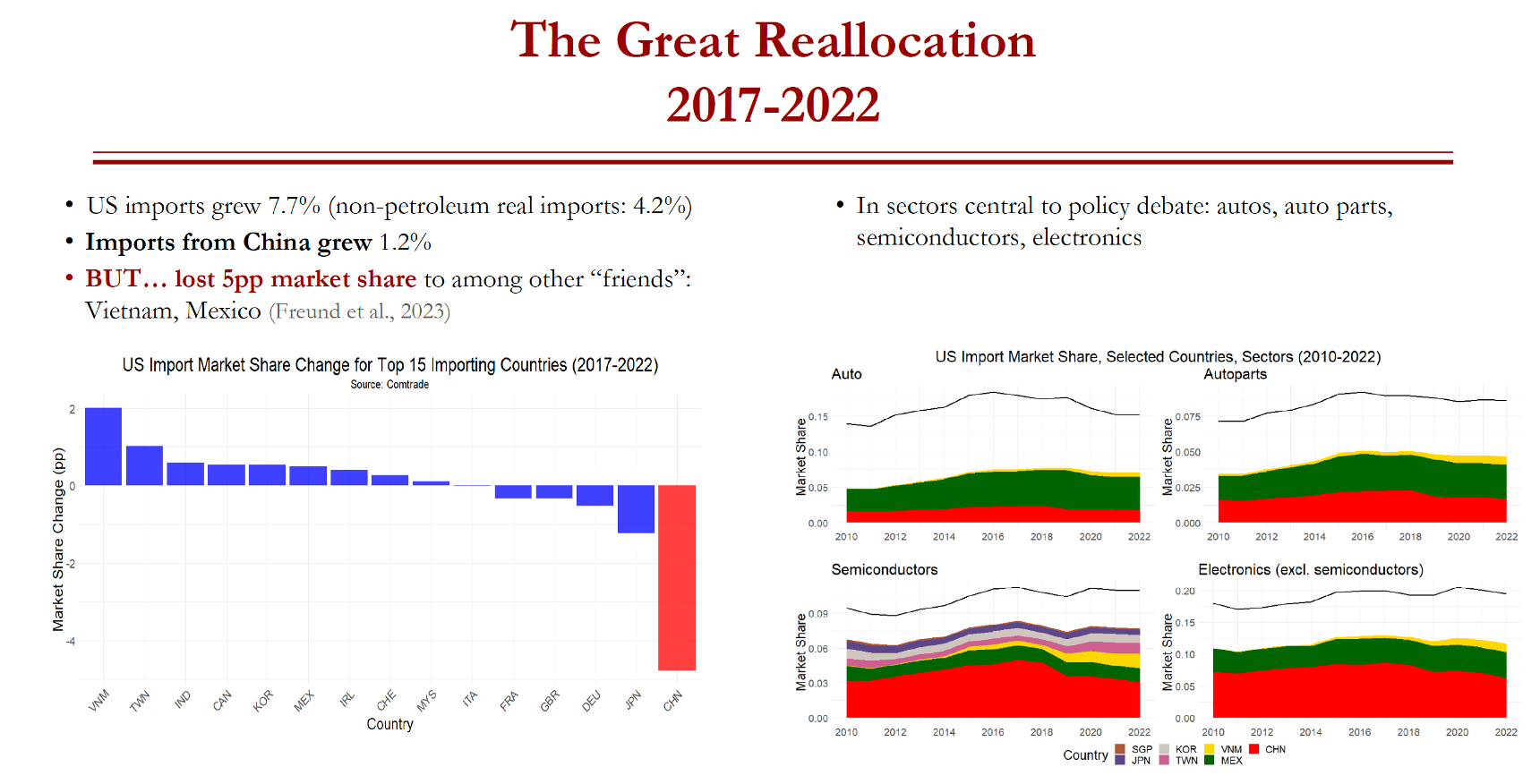

Moreover, as a paper delivered to the 2023 meeting at the Jackson Hole Economic Symposium organised by the Federal Reserve Bank of Kansas City reported, something else important has been going on in US-China trade. In their paper Laura Alfaro of Harvard Business School and Davin Chor of the Tuck School of Business described not deglobalisation nor even decoupling but rather what they termed “the great reallocation”.

In response to the tariffs and other geopolitical factors, US supply chains appear to have adjusted quite rapidly, as have the production sites of Chinese suppliers. The result is shown on this somewhat complicated graph, but I can simplify such a detailed message by saying that what the paper showed was this:

1) there has been a fall in US direct imports from China

2) there has been a corresponding increase in US imports of the same products from other countries, notably Vietnam and Mexico

3) there has been an increase in Chinese firms’ foreign direct investment in those two countries

4) America’s overall trade deficit did not change materially during the period studied.

In other words, supply chains adjusted, but the overall level of international connectedness remained more or less intact. In this case, it was therefore not a case of deglobalisation as such, nor particularly a case of de-coupling (or de-Chimerica-ing), but rather one of reallocation.

This does not tell us whether this “reallocation” was good or bad. The re-routing of supply chains may or may not have raised costs and added to inflation during the period studied. What it tells us is something that should be obvious but often isn’t, especially when discussion of the world’s two great economic and military powers is concerned: the world is not a binary construct, between the US and China.

(The same, strange but seemingly unmoveable binary assumption also used to bedevil discussions of US-Japan economic relations in the 1980s, when that was the hot topic. Americans in particular seemed oddly resistant to the idea that the world consisted of more than just two countries.)

To put it in the language of economics, what is being observed is trade diversion, not trade reduction or destruction.

So it could be said that the first point I want to make about globalisation and its possible future is that the clue is in the name. One of the key characteristics of the post-Cold War era during which this term “globalisation” has become widely used is precisely that a larger and larger range of countries and regions have been participating in the relatively open trade, financial flows and cross-border investments that have become possible.

It is not a matter just of rising trade between a handful of big countries or economic blocs. So now that there are geopolitical tensions between the world’s two largest economies, resulting in some barriers to their bilateral exchanges, this development alone cannot bring the system to a halt. There are too many options, too many countries, too complicated a matrix of commercial relationships to look at this as a simple matter of a movement being either in one clear direction or of a reversal of that movement.

Commerce, whether in goods, services or finance, is like a river: if it meets a new obstacle then it will flow around it, finding new routes and new levels.

Certainly, a number of policies have been and are being instituted in major trading nations that constitute intended barriers against trade with certain other countries: the Trump-Biden tariffs against China; Japan’s economic security legislation; Biden’s Inflation Reduction Act and Chips Act, both of which introduced large subsidy programmes which favoured firms producing in America; the same is true of the European Union’s “Green New Deal”, and even more so of the new Carbon Border Adjustment Mechanism which is scheduled in 2026 to introduce levies on certain imported carbon-intensive goods such as steel and cement; and most recently the Biden administration has imposed 100% tariffs on imports of electric vehicles from China, and the EU has announced smaller additional tariffs on EVs from China too.

There is a lot of protectionism around, in other words. But does it, in the measures seen so far, amount to “deglobalisation”? Data is naturally not yet available covering the most recent measures, but what we have seen so far suggests that at present the ideas of “deglobalisation” and even more so of “goodbye, globalisation” are rather like the famous comment by the Nobel Prize-winning economist Robert Solow that he could see the computer age everywhere except in the productivity statistics: we can see deglobalisation everywhere except in the trade statistics.

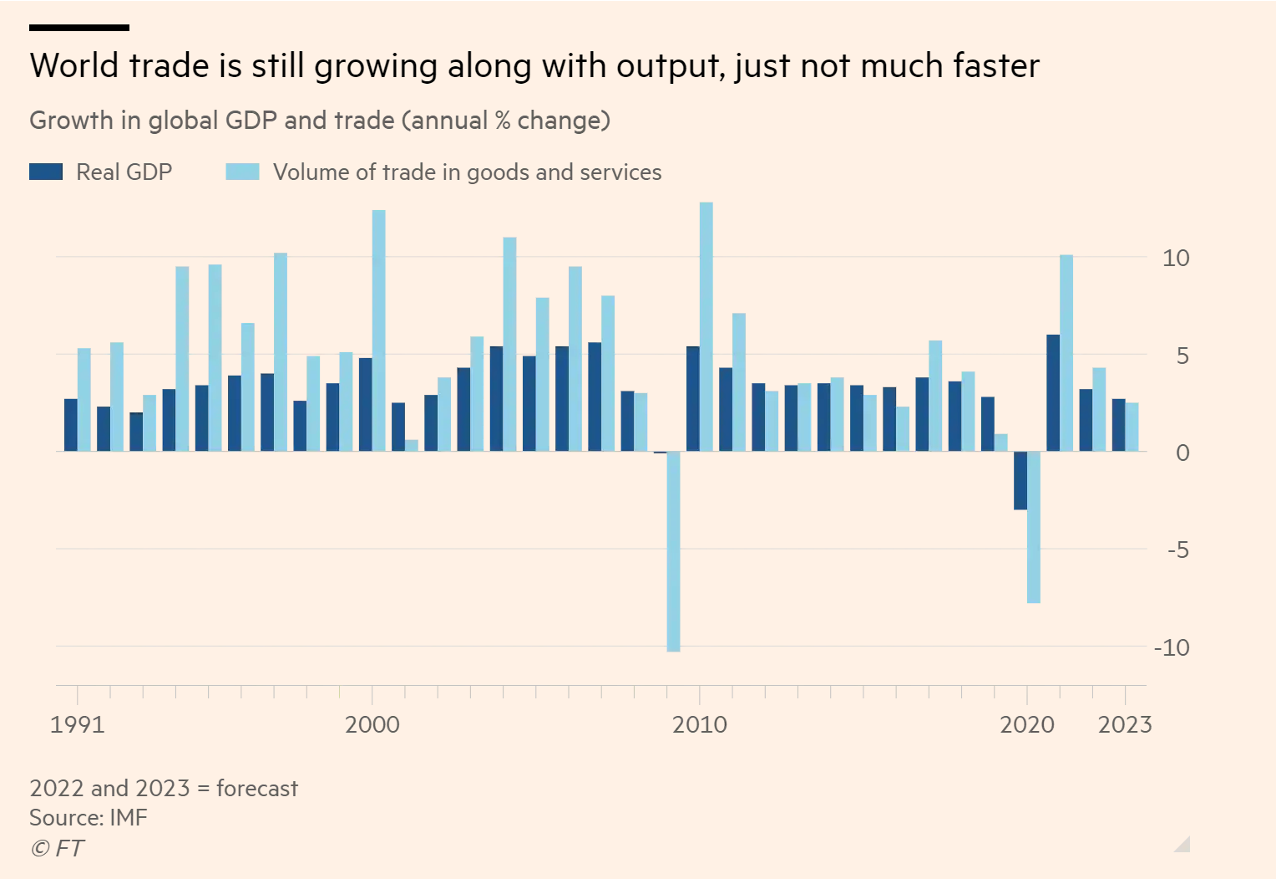

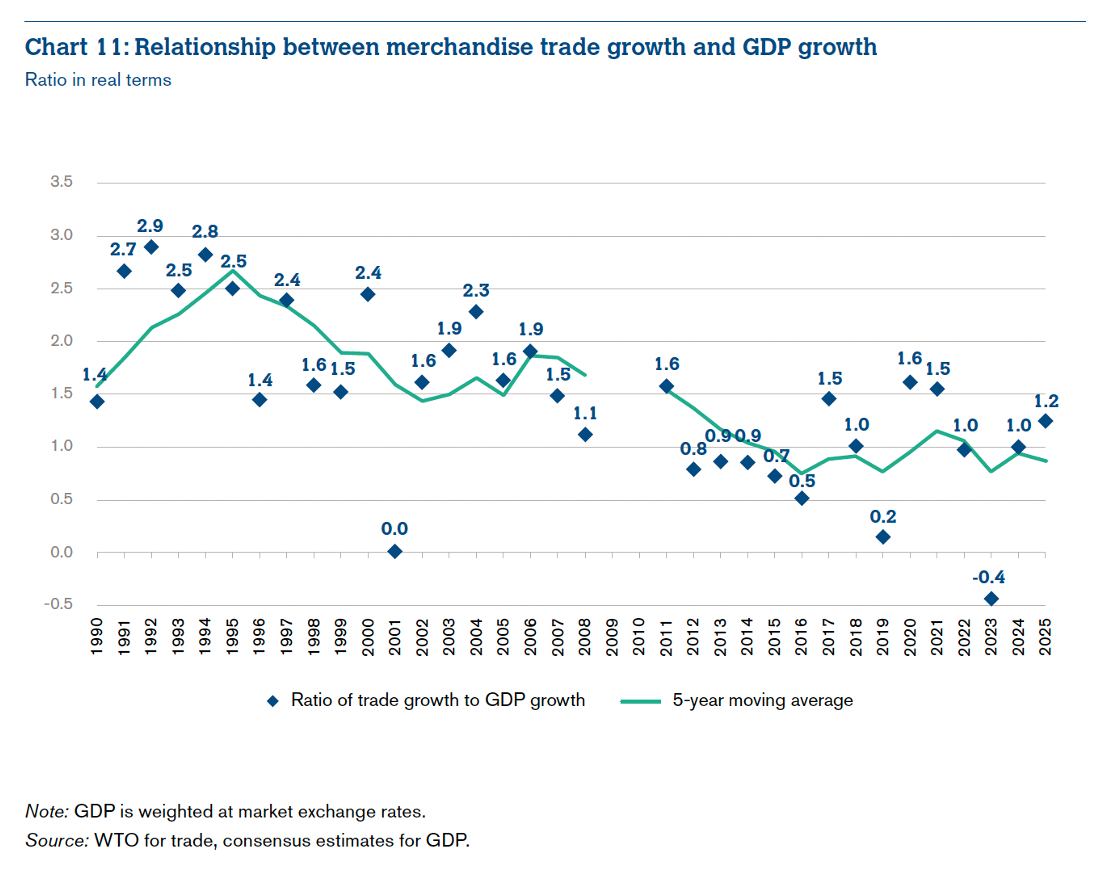

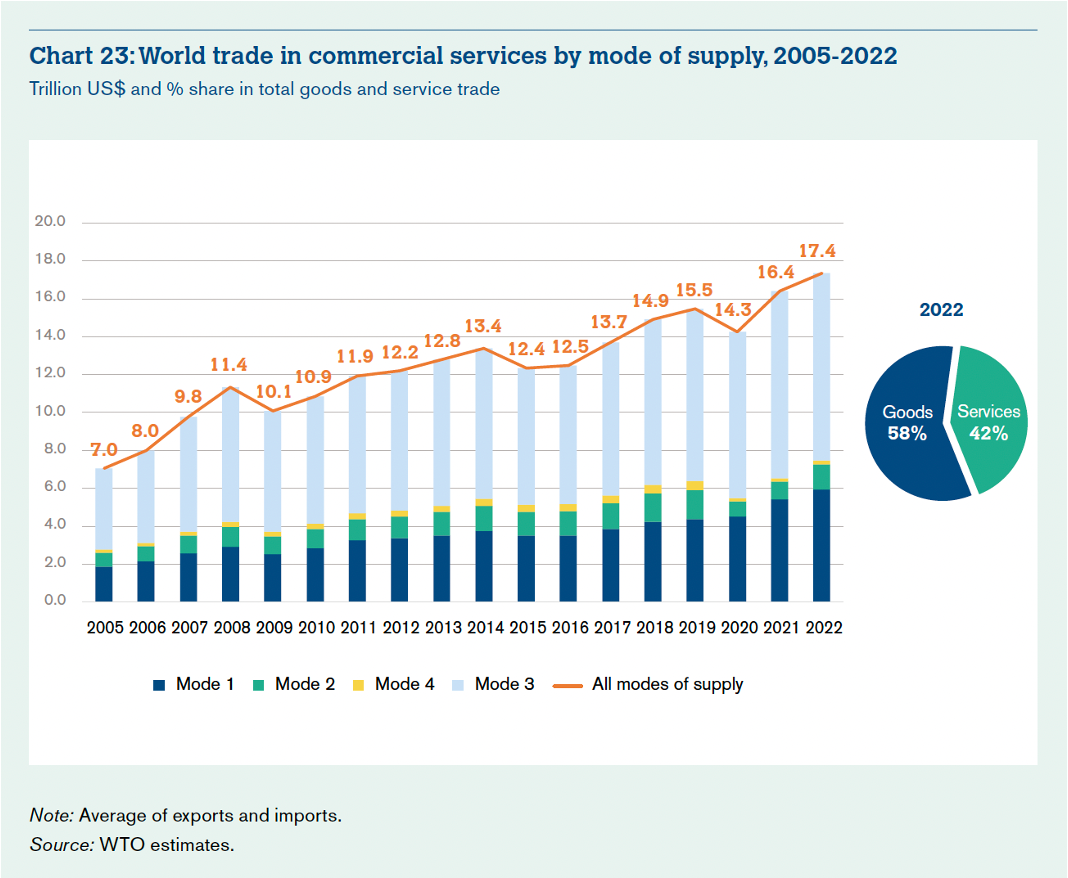

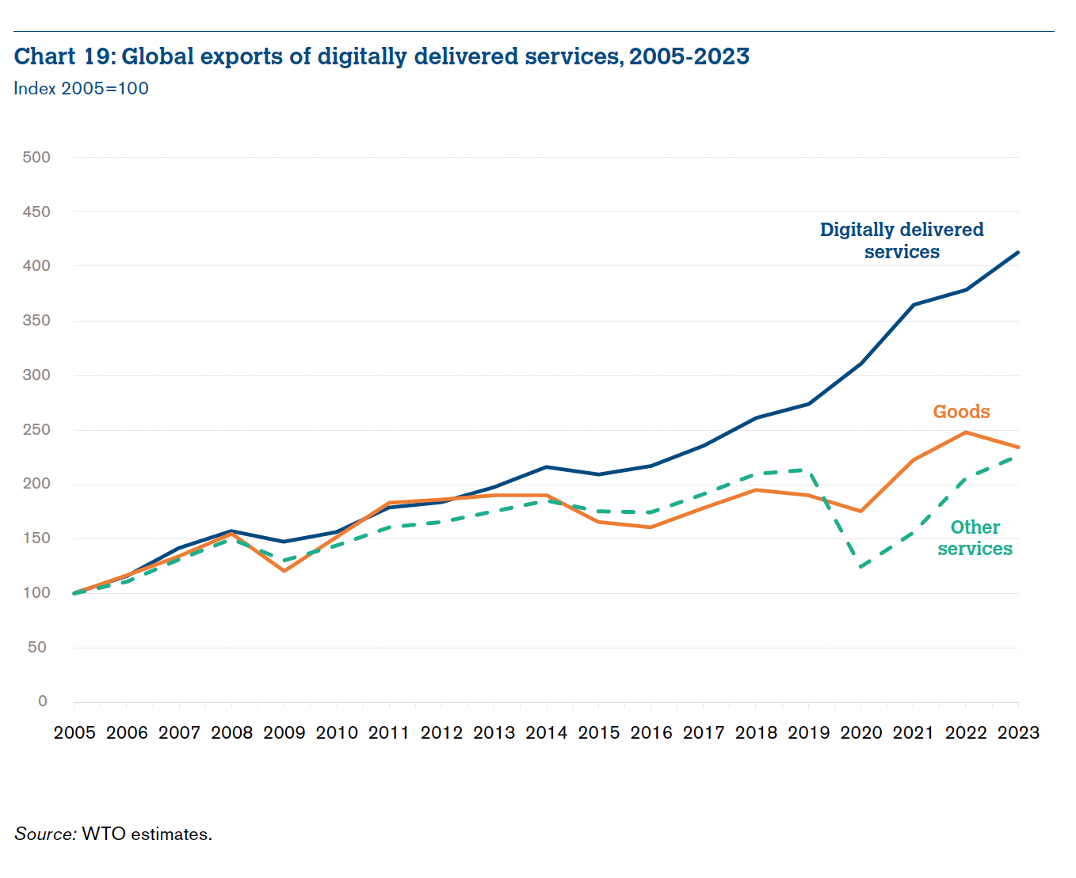

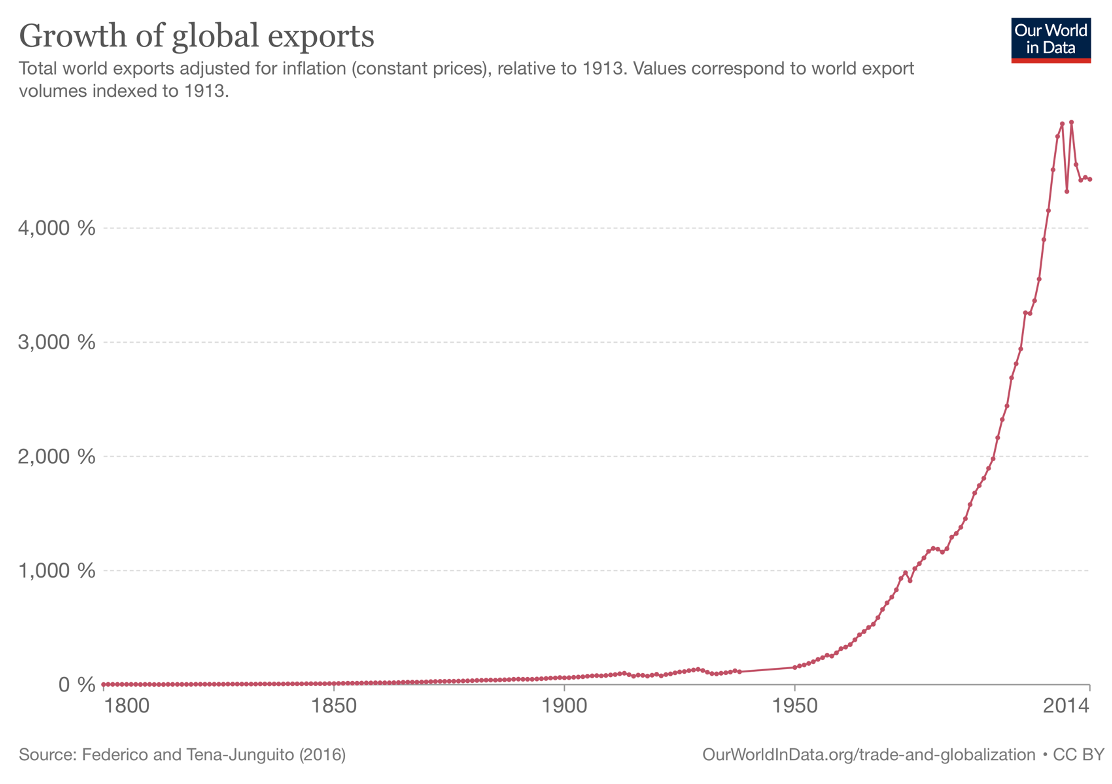

Where better to go for trade statistics than either the (Japanese-owned) Financial Times or the World Trade Organisation? So let’s see if we can spot deglobalisation in these graphs:

No. Neither trade nor GDP are growing as fast as they used to, but both are still growing.

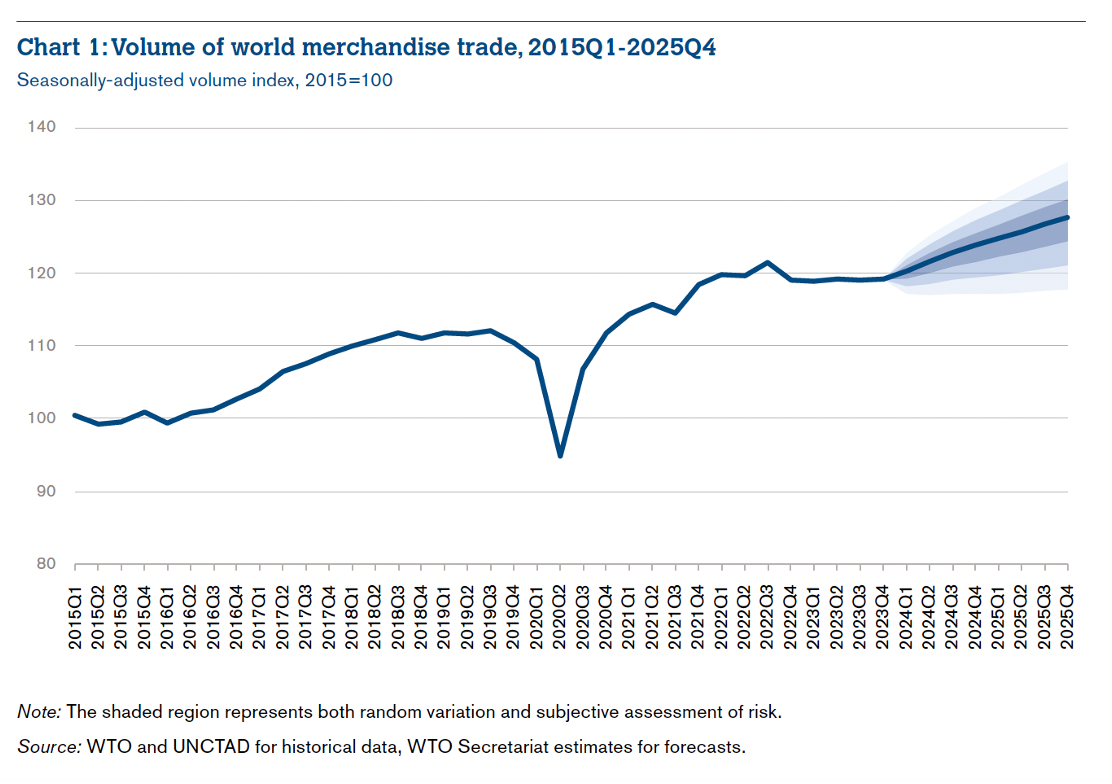

No: definitely still growing there.

Again: still a positive relationship, whether causal or correlative.

Now, that looks rather more like globalisation than deglobalisation.

And the same is true, even more so, for digital services. There’s no deglobalisation in the cloud, at any rate not yet.

Let’s call it the deglobalisation paradox: everyone is talking about it, but there is no sign of it happening, in an aggregate way. In these and the other graphs I have shown we do see change: we see a period in which world trade in goods grew far faster than world GDP, but now their growth is more aligned; we see the diversion of trade thanks to geopolitics and formal barriers, but not its reduction; we see services, especially digitally delivered services, taking over from manufacturing and commodities as the leading force in trade growth.

Richard Baldwin, Professor of International Economics at IMD Business School in Lausanne, Switzerland, who I think it is fair to say is one of the leading analysts of globalisation writing today, has argued in his 2016 book “The Great Convergence” and in a series of articles for the Centre for Economic Policy Research, that recent trends before the war in Ukraine reflect two big things:

first, a period of “offshoring” of manufacturing to China and new emerging markets in the 1990s and 2000s, followed by a new equilibrium in the 2010s and beyond as those emerging markets came to consume a much higher proportion of their own manfactures;

second, an increasing role for information technology in making knowledge a prime ingredient of trade.

That period of offshoring in the 1990s and 2000s is sometimes known as “hyperglobalisation”, as trade expanded a lot faster than GDP, but on Baldwin’s analysis that had more to do with the combination of China’s evolution and the impact of information technology on the way American, Japanese and European firms were now able to operate than on anything inherently good or bad about globalisation. It was an adjustment period, in other words.

The New York Times columnist Thomas Friedman wrote a book in 2005 saying that “The World is Flat”, thanks to the digital revolution, and Baldwin’s analysis, and those WTO statistics on digitally delivered services, confirm that two decades later this is coming true.

Perhaps you might think, with some justice, that I have used a sledgehammer to make this point: that as things stand today, deglobalisation is not happening.

International connectedness is highly affected by geopolitics, but it remains a dominant force in the world economy and indeed in the creation of new ideas and technology. But this does not guarantee that it always will be, nor that the “deglobalisation” theories will necessarily always be wrong.

Having looked at very recent history, let us instead take a look at a longer span of history to try to identify the forces that do make a difference to “the future of globalisation”.

Here is a history of globalisation in a nutshell:

There has always been trade, but really until the 19th century it did not count for much. And even the boom in trade in that century was meagre compared with what happened in the 20th and 21st centuries.

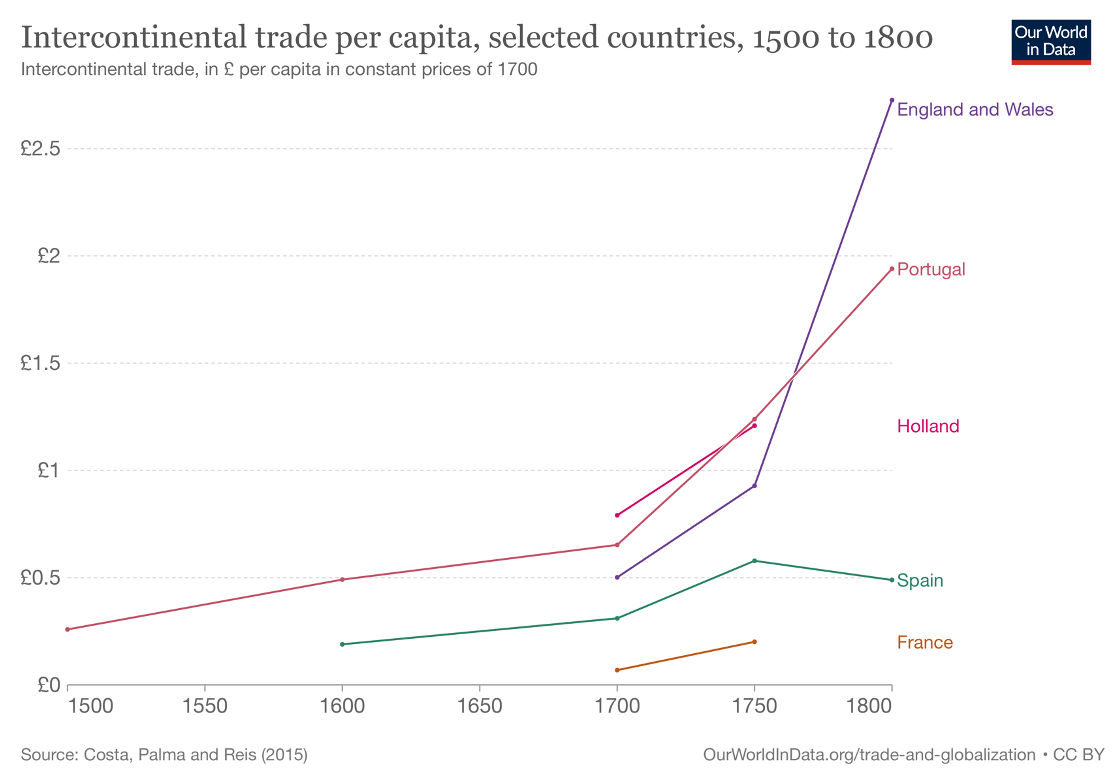

Prior to the 19th century, international trade was significant only when it came attached to empires, which by that era were mostly European: first Portugal, then Spain, then Holland, then Britain. And that brings two clues for the future: the reason why these countries became prominent traders is that they achieved technological leadership in sailing ship design and in weaponry; and then geopolitics, in the form of wars between those European powers and between them and their target countries that later became colonies or settlements like the US that became independent, began to determine the shape and growth of trade.

But it was only the industrial revolution, in the form of steam power and the use of iron and steel, that really began what we can now recognise as globalisation. Some economic historians date this from 1820, a point when domestic price levels in Britain came to be set by international demand and supply, though as a process it had naturally developed over some time.

Here, however, is an important theme: globalisation is driven by a combination of politics and technology. And the force that is too often forgotten or downplayed is technology.

In the European-dominated world of the 19th century, the influence of politics was that war between the European powers took a lengthy pause, between 1815 when Britain defeated France, and 1870, when Germany invaded France for the first time. That peace became correlated with the reduction of tariffs on trade, led by Britain – though not followed by the then rising but still small power of the independent United States.

This period is often known as the first great wave of globalisation. It also produced the first prominent forecast, or at least theory, of the future of globalisation, when in 1912 an English author called Normal Angell wrote a book called “The Great Illusion”.

In it he argued that the new commercial interconnectedness of nations, by which he of course mainly meant European nations, meant that war could no longer be pursued for commercial advantage. And that such were the mutual interests in trade that war really no longer made any sense, at least between the new industrialised powers.

This idea matched a notion that half a century earlier had been propagated by another Englishman, Richard Cobden, himself a cotton-manufacturer who was even involved in the founding of The Economist in 1843 as part of the campaign for free trade.

Cobden argued that freer and more extensive trade between nations was the best way to preserve and extend peace. Angell’s argument in the early 20th century was that this process had gone far enough in Europe to make old causes of war no longer rational.

This may have been true, in a sense, but now counts as the first great bad forecast about the future of globalisation. The start of the First World War, as we now call it, in 1914 when Germany invaded Belgium and France, brought an end to the first great wave of globalisation. Old causes of war turned out to have been superseded by new causes. Four years of war brought great destruction to European economies too, as well as to their commercial relations.

The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery on his doorstep.

In what was by 1919 his most notable book, “The Economic Consequences of the Peace”, the great British economist John Maynard Keynes wrote this lament at what, at least for the English elite of which he formed part, was by then a lost world. For Keynes, life before 1914 sounds the telephonic equivalent of using Rakuten Ichiba or Amazon today.

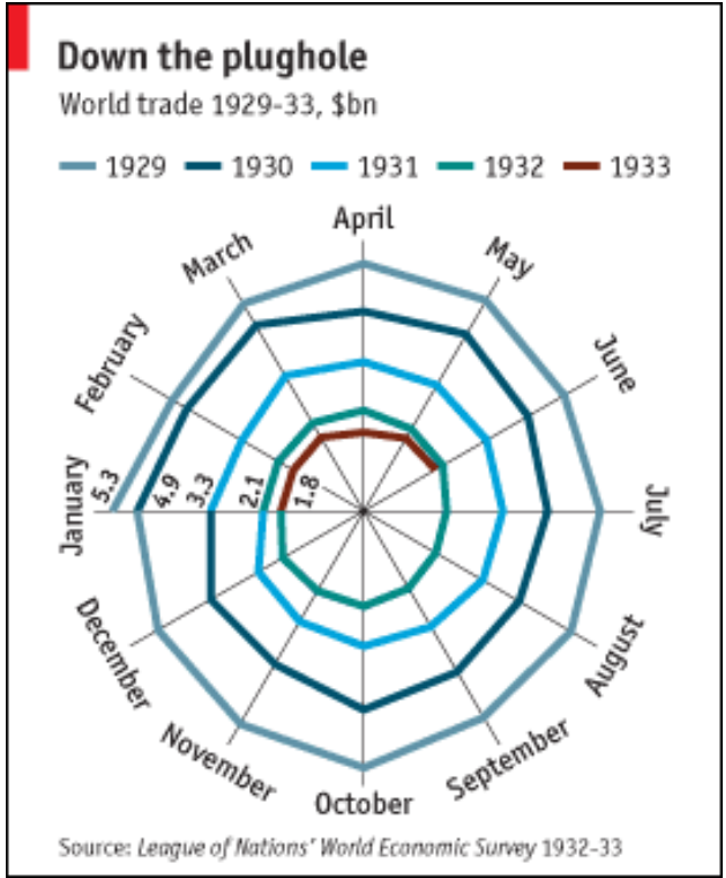

Technology had continued to make progress, in shipping, aviation and telephony. However the 1914-18 war had destroyed three empires which previously had facilitated trade: the Austro-Hungarian empire, Turkey’s Ottoman empire, and the Russian empire which ended in the Bolshevik revolution. Through the financial punishments that the victors imposed on the losers, the war also greatly impeded international finance of all kinds as well as postwar economic recovery. And then, after the technology driven US economic revival in the “roaring Twenties”, the Wall Street crash and banking collapses led to the Great Depression and a trade war, led by huge American tariff increases in 1930.

The world economy was still highly interconnected, which is why US banking collapses also brought down banks and stockmarkets in Europe. But the outcome was definitely a trend of deglobalisation in the form of a sharp contraction in world trade in the 1930s.

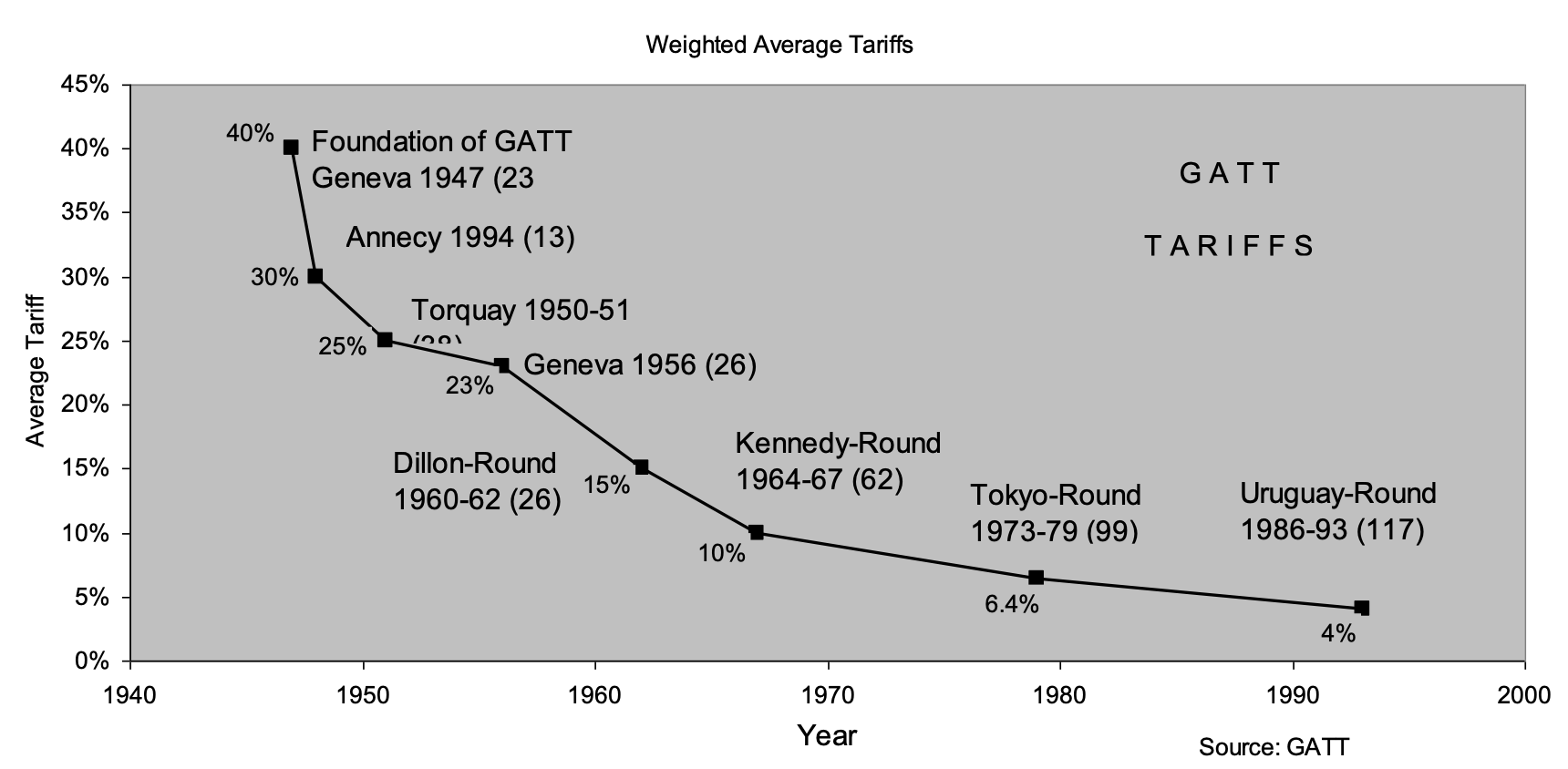

Then, as we all know, came the Second World War, including the Sino-Japanese war. Following peace in 1945, the victorious powers established the General Agreement on Tariffs and Trade in 1947 to begin a process of reducing tariff barriers and setting common rules, and financial institutions including the IMF, the World Bank and a new exchange-rate system to try to stabilise finance.

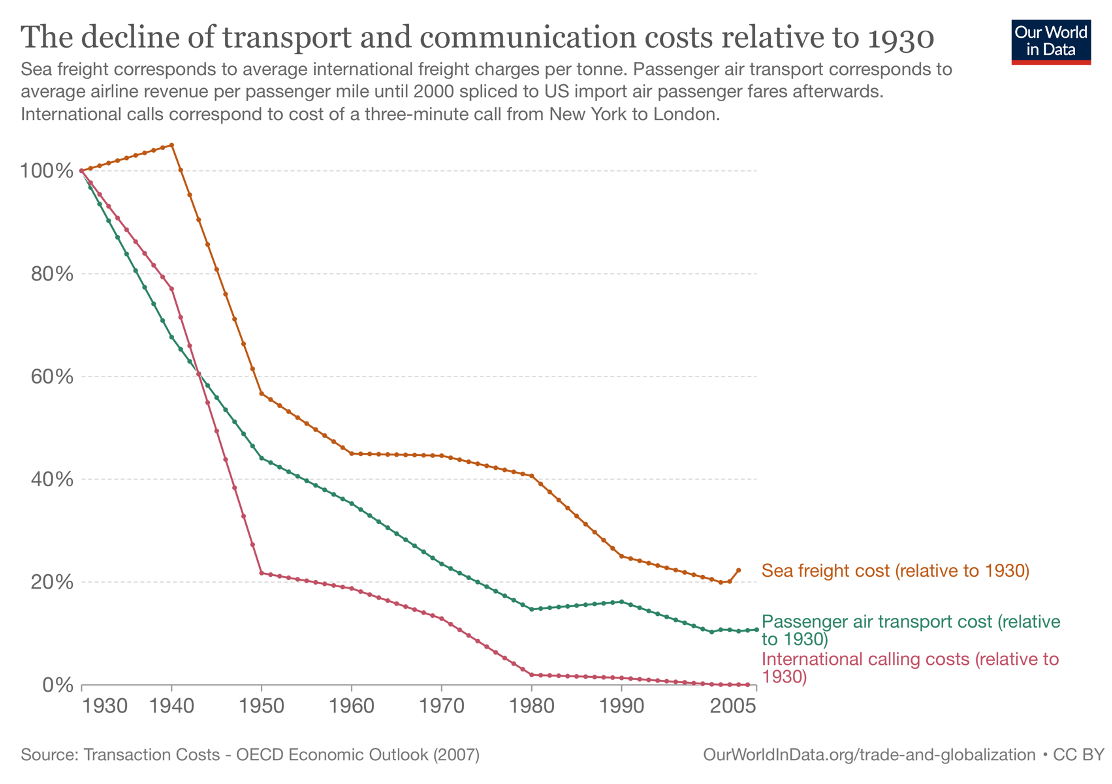

The result was a new boom in trade, albeit in a world that became divided by the Cold War. Politics enabled that boom, but what is often not recognised is that technology played a huge role too.

It used to be said in the era of imperial commerce that “trade followed the flag”. Given the role played by the dramatic falls in shipping, aviation and telecommunications costs during the 1950s and beyond, especially following the adoption of containerisation, we might reasonably say that during the postwar era “tariff policy followed the trade”. The technological forces driving international trade acted as an enabling factor for tariff reductions and eventually, in the post Cold War 1990s, for the universalisation of trade rules and relatively low tariffs under the newly established World Trade Organisation.

This brings us to the era now known as the heyday of globalisation. Japan had in reality been one of the earliest beneficiaries of globalisation during its high-growth period of the 1960s, 70s and 80s, but then China became the symbolic centre of post-cold war globalisation.

Even in that heyday, there were efforts made to describe or prescribe the future of globalisation. I will discuss them briefly, as I think they can be instructive.

The first emerged from the US-Japan “boeki masatsu” or trade friction of the 1980s. The Economic Strategy Institute, a think-tank founded in Washington, DC, by Clyde Prestowitz, a former US Commerce Department official, came to stand for replacing free trade, as it saw it, with “managed trade”, as was advocated in this 1990 paper by his colleague Robert Kuttner.

In some ways, the US-Japan friction had indeed led to “managed trade” through the “voluntary restraint” agreements and other measures between Japan and the US. But whatever the policy-related arguments, the 1990s did not turn out to fulfil Kuttner’s prescription.

Most of all, the idea of “managed trade” really reflected an idea of a binary key trading relationship between what were then the world’s two largest economies, the US and Japan. But as I have already argued, this focus on bilateral trade fails to understand the now multilateral nature of trade in goods and services. Perhaps, to be fair, Kuttner and Prestowitz were making this argument before the impact of IT on supply chains was becoming evident and before the world became as complicated as it did from the 1990s onwards. Nonetheless, a very similar argument is being made today by the man who was Trump’s US Trade Representative during his first term, Robert Lighthizer, that the threat from China makes “managed trade” both essential and inevitable.

Japan’s own great Kenichi Ohmae was and is much more in favour of globalisation, what he called “a borderless world”, than Kuttner. In this 1995 book, “The End of the Nation State: the Rise of Regional Economies”, he can be said now, three decades later, to have been both right and wrong.

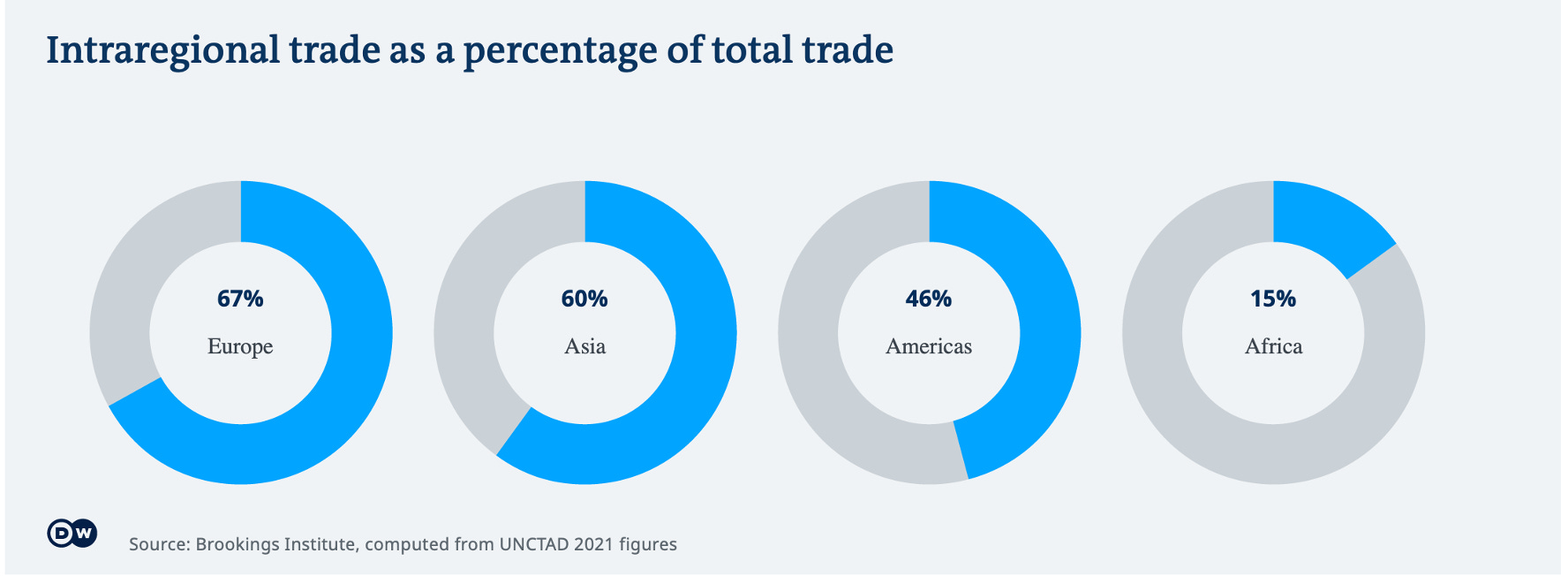

He was right to observe that as trade barriers were lowered and previously self-isolated countries like China, India and others chose to join the world economy, so the natural bias of commerce towards trade with neighbouring countries would be able to assert itself. Paul Krugman’s 2008 Nobel prize was won for his 1979 work on how scale and other factors gives trade strong geographical biases, both within cities and between neighbours, if other barriers do not get in the way.

As this chart shows, intra-regional trade has become extremely important as a share of total trade both for Europe and for Asia. Much slower progress in achieving regional free trade agreements explains why Africa and the Americas show lower shares for intra-regional trade.

Where with hindsight we can say that Ohmae was wrong was in giving this “regionalisation” such a dominant role at a time when other factors were also encouraging supply chains to be extended far beyond simple regions, as IT enabled firms to combine their management knowhow with cheap wages in countries far away. “The World is Flat” changed things in ways that Ohmae, writing in 1995, could not have anticipated. Globalisation has not, so far, turned out to mean regionalisation.

Nonetheless, the idea that the future lies in regional trading blocs is a highly persistent one. This paper from the Carnegie Endowment for International Peace in 2010 is just one example.

Again, the idea contains some clear elements of truth, elements which have if anything become stronger as time has passed. Progress in renewing trade agreements at the multilateral level of the WTO has become essentially frozen, and the WTO dispute settlement system itself has been undermined by America’s blocking of new members for the arbitration panels. So regional agreements – paramount among them recently the CPTPP in the Asia-Pacific, but also a new deal in Africa and the ever-influential European Union – have become the name of the game in the setting of trade rules and standards.

This focus on the regional level as the place for settling rules, disputes and standards looks fairly well set, given the troubles of the WTO. But we should still be cautious in using that tendency to predict the future of a phenomenon as complex as globalisation.

The reason we should be cautious is that at current levels of trade barriers, regional trade agreements are important without being decisive. These “blocs” are important politically, but companies nonetheless find it perfectly possible to conduct trade, within their supply chains, across multiple blocs. Only if they became far more exclusive, with more severe and costly barriers, would they really obstruct globalisation. They do surely cause some trade diversion. But they are not the only force in play.

Let me now make some concluding points, that indicate the way in which I believe we should be thinking about the future of global commerce and the process we have called “globalisation”.

The history of globalisation that I have outlined has shown the development of international trade in goods and services to have been driven by three main forces:

Peace, war and international security

National external trade policies

Technology, and its effect on transaction costs

It is clear that the biggest discontinuity in the growth of international commerce was caused by what we now know as the two world wars of the 20th century.

Russia’s invasion of Ukraine in 2022 has certainly diverted trade and financial flows considerably, thanks to direct security effects and to sanctions. But neither it nor the other conflicts we can see occurring in the Middle East, Africa or elsewhere have been sufficient to block global trade in a significant way.

Tensions between the US and China similarly have some diversionary effects, and are to some degree echoed in tensions between China and Europe and China and Japan. But those geopolitical tensions would have to get a lot worse to have a major effect on global commerce as a whole, in part because the world economy has become much more complex and multipolar in nature.

The one conflict that would be very likely to have a major “deglobalisation” influence would be a conflict between the US and China over Taiwan, for such a conflict would very likely reach catastrophic proportions and would force many countries to choose sides. We cannot predict how commerce and the exchange of ideas would look after such a conflict, just as my European forebears would have been unable to predict the world after 1918 from the standpoint of 1914 or earlier.

Secondly, nations’ external trade policies. As I commented earlier, there has been a clear trend back towards protectionism since the 2008 financial crisis, one that has lately been reinforced by policies aimed at the energy transition and by US-China tensions.

This has not yet however had a major effect on world trade. It could, of course. The big question is what would happen if Donald Trump is re-elected as US President in November and carries out his promise to impose a 10% tariff on all imported goods, and a 60% tariff on all goods from China.

One quite likely possibility is that other countries – including the EU, the UK, Japan and indeed China – would retaliate by imposing higher tariffs of their own, and we would be in a trade war, one that could escalate higher and higher.

The wider such a trade war became – ie, taking in more countries – the likelier it would be to make deglobalisation visible in the trade statistics. Nonetheless, we should bear one other thing in mind: this is that services, especially digitally delivered services, have become an increasingly important component of global commerce. How they would be affected is unpredictable.

Third, we need to bring in the related and vitally important force of technology. Falling costs and increasing digital capabilities have been a big factor behind the growth of global commerce. The entry of artificial intelligence means that there is no likelihood of this technological force for cross-border commerce diminishing.

During the pandemic, the science and technology behind vaccine development, production and distribution were all global, even if geopolitics introduced some distortions. Moreover, the basic reason why the US stockmarket has been driven by the so-called “Magnificent Seven” tech stocks is that the market for all of them is global.

Geopolitics threatens, but as yet it does not decide. External trade policies at present divert, but only an escalatory trade war would be likely to have a major effect. Technology, however, remains the most powerful force in favour of continued globalisation.

The future of globalisation will be determined by the interplay of these three forces. There is no currently pre-determined destiny for globalisation. Many commentators over-play the influence of politics and under-play the role of technology. Extreme outcomes are possible, and need to be prepared for. But we must above all keep an open mind as to what the actual outcome will be.

THANK YOU FOR LISTENING, LADIES AND GENTLEMEN